Your consolidated statement looks clean until an auditor finds a $500,000 variance. Over half of all companies still handle intercompany transactions manually. This manual work increases consolidation risk and slows the financial consolidation process.

Most finance teams struggle with human errors during the close. These errors often come from poor intercompany matching. You can fix these issues by automating your intercompany elimination steps.

This guide explains how to manage intercompany transactions to protect your business. We look at intercompany reconciliation and how to handle intercompany payables and receivables before the audit starts.

Why intercompany transactions fail long before consolidation runs

Your consolidation error is just a symptom. The real break happens weeks earlier. It starts when entities record and match intercompany transactions differently.

This creates a hidden consolidation risk that ruins your month-end close. You must track intercompany transactions properly from the start to avoid surprises.

1. Timing gaps in record keeping

Subsidiary A records a sale for intercompany transactions in March. Subsidiary B records the cost in April. This creates a timing gap. This gap breaks your intercompany reconciliation. Both sets of books look fine on their own.

However, the gap creates an imbalance in your intercompany payables and receivables. This is a common issue in multi-entity accounting.

2. Misaligned chart of accounts

Each entity might use a different chart of accounts. If account codes do not match, you cannot use automated intercompany matching. Your team spends days manually mapping accounts. This makes your financial consolidation process much slower. You need a uniform structure to manage intercompany transactions across the group.

3. Hidden profit in inventory

When one entity sells to another at a markup, profit stays internal. This is an unrealized profit. Both IFRS 10 and ASC 810 demand an unrealized profit elimination.

This is a key part of your intercompany elimination strategy. If you fail to do this, you report money you haven’t truly earned from external customers.

These errors create significant problems that build up over time.

The consolidation risk that builds up when intercompany transactions go unmanaged

Ignoring mismatching intercompany transactions creates more than just a small math error. It builds a dangerous consolidation risk that threatens your entire audit.

You must treat intercompany transactions as a primary concern to keep your financial consolidation process safe.

If you don’t, you face four major failure modes that hurt your bottom line.

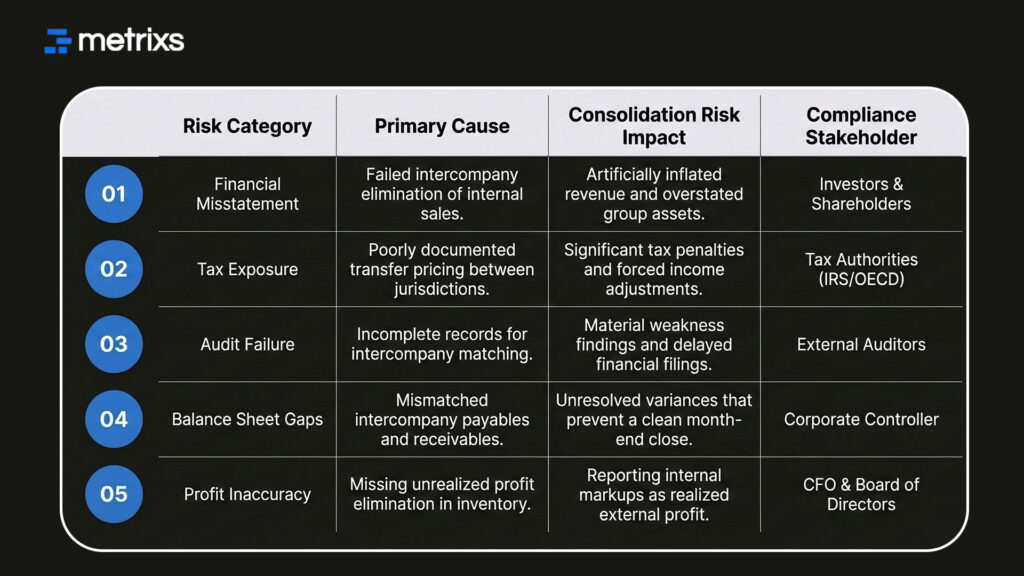

1. Artificially inflated revenue and assets

When you skip a full intercompany elimination, your internal sales show up as external growth. If a parent company sells to three subsidiaries for $500,000, your consolidated statement might record that as real revenue.

This is wrong. No external customer paid that money. This mistake overstates your group’s success and inflates your assets. It presents a false picture to your investors.

2. Transfer pricing exposure across jurisdictions

Entities in different tax regions must price intercompany transactions at arm’s length. This means the price must match what a stranger would pay. If your transfer pricing is not documented, tax authorities will notice.

They can adjust your taxable income and charge heavy penalties. This risk grows every time you move goods or services across borders.

3. Audit findings from incomplete records

Both ASC 810 and IFRS 10 require strict proof for every intercompany elimination. You need a clear trail of who matched the balance and when they did it. Manual processes often lack these detailed records.

This leads to audit findings that delay your filing. Even if the final numbers are right, a messy audit trail creates regulatory exposure for your team.

4. Imbalances in intercompany payables and receivables

A common consolidation risk involves mismatched intercompany payables and receivables. If one entity records a debt and the other doesn’t, the group balance sheet won’t zero out.

This forces your team to hunt for the error during the final close. These imbalances often stem from poor intercompany matching at the entry level. This makes your intercompany reconciliation a nightmare every single month.

Table for consolidation risk matrix: The impact of unmanaged transactions

Fixing these issues requires a change in how you handle data before the close begins.

What fixing intercompany transactions actually requires before consolidation

Fixing intercompany transactions is not just about a final check at the end of the month. You must change your workflow at the start. Most finance teams try to fix intercompany transactions during the final close.

This is too late. You need a structural fix for your financial consolidation process to work smoothly.

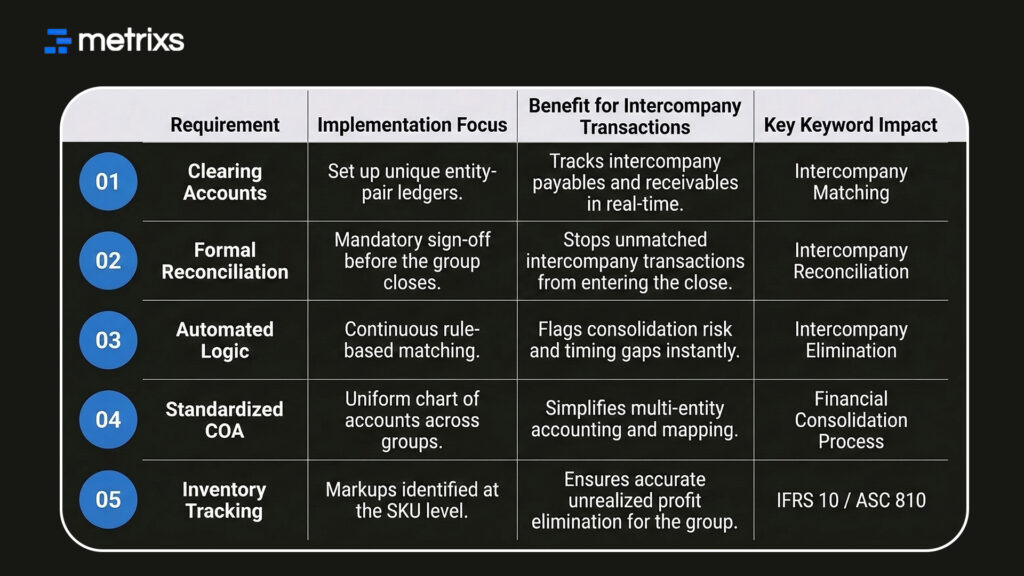

1. Clearing accounts and matching logic

Set up dedicated clearing accounts for every entity pair. This creates an internal ledger to track intercompany transactions as they happen. When you post to these accounts in real time, you catch gaps immediately.

This logic helps with intercompany matching before the data ever reaches the consolidation layer. It ensures your intercompany payables and receivables stay in balance from day one.

2. Pre-consolidation reconciliation as a formal step

Make intercompany reconciliation a mandatory task before the group close starts. Each entity must confirm their balances with their counterparts. This stops one subsidiary from closing while another still has open entries.

If you treat this as an informal check, you invite consolidation risk. Formal sign-offs ensure that multi-entity accounting data is clean and ready.

3. Automation for real-time exception flags

Use software to flag mismatches in intercompany transactions immediately. This automation identifies currency conversion errors or price differences before they cause a problem.

It routes these issues to the right person for a quick fix. We prevent the usual month-end scramble for your team. Real-time flags provide the audit trail required by ASC 810 and IFRS 10.

4. Standardized chart of accounts across the group

A uniform chart of accounts is the backbone of successful intercompany transaction management. When every entity uses the same codes for internal sales, intercompany matching becomes instant.

You stop wasting time translating data from different systems. This consistency is the most effective way to handle intercompany elimination without manual effort.

Table for strategic requirements for pre-consolidation accuracy:

These steps prepare your data so that tools like Metrixs can finish the job faster.

How Metrixs fixes intercompany mismatches before they reach consolidation

Metrixs fixes intercompany transactions by automating your financial consolidation process within Microsoft Dynamics 365. It provides 99.9% data accuracy and 80% faster reporting. This tool removes consolidation risk by providing clear oversight of intercompany payables and receivables.

Key strengths:

- Rapid integration: Deploy a seamless intercompany elimination strategy in under six weeks.

- On-demand snapshots: Use real-time data for proactive intercompany matching decisions.

- Multi-region flexibility: Track multiple currencies to ensure consistent reporting for intercompany transactions.

- Centralized oversight: Automate financial summaries to reduce manual work and human error.

Metrixs turn data into a competitive advantage for your group. Explore how Metrixs ensures you use your ERP to its full advantage and simplifies your intercompany transactions → Metrixs

Conclusion

Fixing intercompany transactions before your final close is the only way to reduce consolidation risk. When you manage intercompany payables and receivables manually, you face constant errors and timing gaps.

These discrepancies stall your financial consolidation process and force your team into a high-pressure, last-minute scramble. If you fail to resolve these mismatches, you risk reporting inflated revenue and facing severe audit failures.

Inaccurate intercompany elimination can trigger regulatory penalties and damage your market credibility permanently. You cannot afford to leave these balances unverified.

Metrixs provides the automation needed for real-time intercompany matching and accurate reporting. It ensures your data meetsASC 810 and IFRS 10 standards without the manual rework.

Let’s connect with Metrixs and simplify your intercompany transactions to protect your business from consolidation risk today.

FAQs

1. What are intercompany transactions, and why do they need to be eliminated?

Intercompany transactions are internal exchanges like sales or loans between entities. You must perform an intercompany elimination because consolidated statements only show external activity. Without this, internal transfers inflate revenue and assets, creating a false financial consolidation process that ignores real consolidation risk.

2. What is the difference between intercompany reconciliation and intercompany elimination?

Intercompany reconciliation is the matching phase where you verify intercompany payables and receivables. In contrast, intercompany elimination is the actual removal of those matched balances. Proper intercompany matching must happen first to ensure your multi-entity accounting results are accurate and audit-ready.

3. What does ASC 810 require for intercompany transactions in consolidated statements?

ASC 810 requires a group to report as a single economic entity. This means all intercompany transactions, including unrealized profit elimination from inventory, must be removed. Ignoring these rules creates a major consolidation risk and leads to significant financial reporting errors.

4. Why do intercompany transactions create transfer pricing risk?

Cross-border intercompany transactions must follow transfer pricing rules at arm’s length. If your intercompany matching is messy, tax authorities may adjust your income and levy penalties. Accurate intercompany reconciliation ensures your group stays compliant with international tax laws and regulatory standards.

5. How does automation reduce consolidation risk from intercompany transactions?

Automation uses real-time intercompany matching to flag gaps in intercompany payables and receivables instantly. This reduces consolidation risk by catching errors before the financial consolidation process ends. It provides the clear audit trail required by ASC 810 and IFRS 10 mandates.